Police Freeze Your Bank Account UK | What Happens & Your Rights

What Happens If Police Freeze Your Bank Account in the UK?

🎧 Listen to the Audio Summary

Can Police Freeze Your Bank Account in the UK?

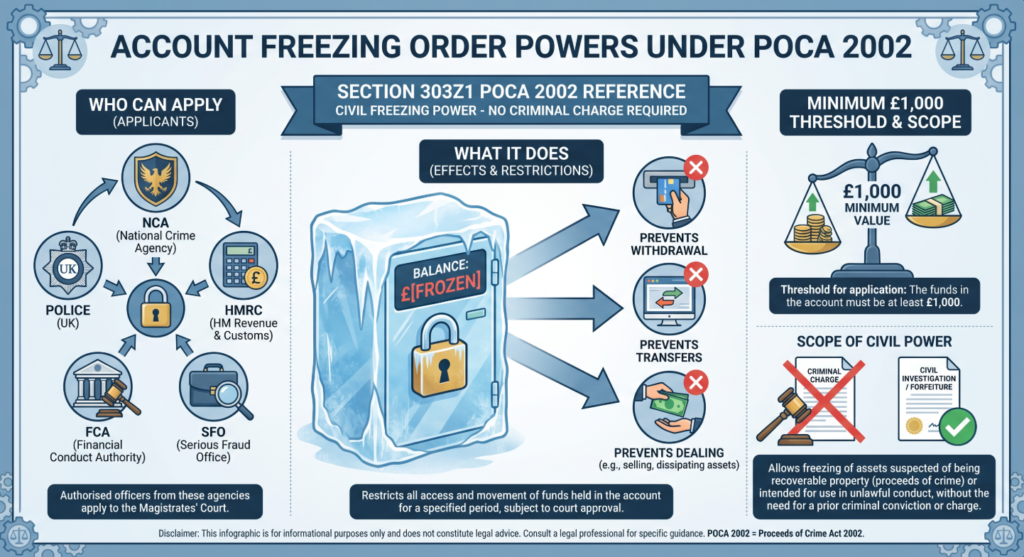

Yes. Police and other authorised enforcement agencies have the power to apply for an Account Freezing Order under Section 303Z1 of the Proceeds of Crime Act 2002, which prevents you from withdrawing or dealing with the funds in your account.

Legal Power

Legislation

Who Can Apply

Account Freezing Order (AFO)

Section 303Z1 POCA 2002

Police; NCA; HMRC; FCA; SFO; Local authorities

Account Forfeiture Order

Section 303Z14 POCA 2002

Same enforcement agencies

Restraint order

Section 41 POCA 2002

Prosecution in criminal proceedings

Civil recovery freezing order

Section 245A POCA 2002

NCA civil recovery

Unexplained Wealth Order

Section 362A POCA 2002

NCA; SFO

What an AFO Does

Effect

Prevents withdrawal

Cannot take money out of account

Prevents transfers

Cannot move money elsewhere

Prevents dealing

Cannot use funds to pay debts

Account remains open

Account is not closed

Incoming payments

May still be credited depending on order terms

Does not mean charged

AFO does not require criminal charge

Who Can Seek an AFO

Authorised Enforcement Officers

Police

Specifically authorised investigating officers

National Crime Agency

Serious organised crime

HMRC

Tax fraud; VAT fraud

Financial Conduct Authority

Financial services offences

Serious Fraud Office

Complex fraud cases

Local authorities

Trading standards; benefit fraud

The Minimum Amount

POCA 2002 Requirements

£1,000 minimum

Account must contain at least £1,000

Below this

AFO cannot be made

Effect

Smaller amounts cannot be frozen under AFO

Why AFOs Are Used

Reasons

Preserve evidence

Prevent dissipation of funds

Protect against money laundering

Stop further movement of criminal proceeds

Alternative to restraint order

Does not require criminal proceedings

Speed

Can be obtained quickly

Low bar

Reasonable grounds to suspect; lower than criminal standard

How Long Can Police Freeze a Bank Account in the UK?

An Account Freezing Order initially lasts for up to 2 years. This is the maximum initial period, but extensions are available.

Duration

Position

Initial AFO

Up to 2 years from date of order

Extension

Further period applied for before expiry

Maximum extension

No statutory maximum on total duration

In practice

Can last several years in complex cases

Review

Can apply to vary or discharge

The Two-Year Period

What Happens

During AFO

Investigation proceeds

No charge required

AFO does not require criminal proceedings

Forfeiture application

Authority may apply for forfeiture during period

End of period

Order expires unless extended or forfeiture ordered

If no forfeiture

Funds released at end of period

If forfeiture ordered

Money permanently taken

Can the AFO Be Extended?

Yes

Application to court

Enforcement authority applies before expiry

Grounds

Investigation continuing; forfeiture proceedings not concluded

You can oppose

Make representations against extension

Solicitor essential

To represent you at extension hearing

No automatic extension

Court must approve

Forfeiture Application Timeline

What Happens Next

During AFO period

Authority gathers evidence

Forfeiture application

Made to magistrates’ court

Standard of proof

Balance of probabilities

If forfeiture granted

Money taken permanently

If not granted

Money returned at end of AFO

What Is an Account Freezing Order Under UK Law?

An Account Freezing Order (AFO) is a civil court order made by a magistrates’ court under Section 303Z1 of the Proceeds of Crime Act 2002, which prohibits a person from making any payment from or dealing with the funds in a frozen bank or building society account.

Key Features of an AFO

Details

Court

Magistrates’ court

Application

Made without notice in most cases

Standard

Reasonable grounds to suspect

Criminal charge

Not required

Civil standard

Lower than beyond reasonable doubt

Duration

Up to 2 years; extensions possible

Effect

Account frozen; cannot deal with funds

The “Reasonable Grounds to Suspect” Test

What Authorities Must Show

Lower than criminal standard

Not beyond reasonable doubt

Lower than civil standard

Not balance of probabilities

Objective test

Would a reasonable person suspect?

Basis for suspicion

Transaction patterns; intelligence; SAR

No proof of crime

Suspicion sufficient

Challenge possible

Grounds can be challenged at hearing

What Happens in the Account

Money During AFO

Money remains in account

Not seized; not taken

Bank holds it

Under court order

Interest

May continue to accrue

New credits

Depending on exact terms of order

Not given to authorities

Unless forfeiture order follows

Returned if no forfeiture

At end of AFO period

Difference: AFO vs Restraint Order

Comparison

AFO

Civil power; no criminal proceedings required; magistrates’ court

Can Police Freeze Your Bank Account Without Telling You in the UK?

Yes. Account Freezing Orders are almost always applied for without notice, meaning the order is made before you are informed, giving you no opportunity to object in advance.

Without Notice Application

Why It Happens

Standard practice

AFOs almost always without notice

Risk of dissipation

If told in advance; money could be moved

Court power

Can make order without hearing from you

When you find out

When bank informs you; or card is declined

First knowledge

Often when trying to use account

What Must Happen After

Your Rights Post-Order

Served with order

You must be served with a copy

Notice of proceedings

Told about any forfeiture proceedings

Right to apply to vary or discharge

Can apply to court to challenge

Hearing

Can be listed to consider your representations

Solicitor

Essential to instruct immediately

Bank’s Role

What Bank Does

Receives order

Bank served with AFO

Freezes account

Must comply with court order

Informs customer

Usually notifies account holder

Tipping off concern

Limited by anti-tipping off provisions in some cases

Cannot disclose SAR

If SAR filed; cannot tell you

Suspicious Activity Reports

How They Relate

Bank files SAR

If suspicious activity identified

NCA receives

Assesses; may disseminate

Can lead to AFO

NCA or police may then apply

Cannot tell you

Tipping off prohibition

Your first knowledge

May be the AFO itself

What Are Your Rights If Police Freeze Your Bank Account?

Despite the without-notice nature of AFOs, you have important legal rights once you become aware of the order.

Right

Legal Basis

What It Means

To be served with order

POCA 2002

Must receive copy of the order

To apply to vary or discharge

Section 303Z9 POCA 2002

Challenge the order in court

To legal representation

Common law; Article 6 ECHR

Represent yourself or instruct solicitor

To apply for living expenses

Section 303Z9 POCA 2002

Release of funds for reasonable expenses

To know the basis

Article 6 ECHR

Must be told grounds for the order

To oppose forfeiture

Section 303Z14 POCA 2002

Challenge any forfeiture application

To appeal

Section 303Z16 POCA 2002

Appeal to Crown Court

Article 1, Protocol 1 ECHR

Right to Peaceful Enjoyment of Property

What it protects

Peaceful enjoyment of possessions

Application

AFO interferes with your property rights

Proportionality

Order must be proportionate

Public interest

Must serve legitimate public interest

Challenge basis

Can argue order disproportionate

Article 6 ECHR

Fair Trial Rights

What it protects

Fair hearing

Application

Right to be heard on AFO and forfeiture

Practically

Right to attend; make representations; be legally represented

Forfeiture proceedings

More significant Article 6 concerns

Who Can Apply to Vary or Discharge?

Standing

Account holder

Primary right to challenge

Third parties

Others with interest in account

Businesses

Where business account is frozen

Joint account holders

Both may have rights

Legal owner

Anyone with legal interest

How to Challenge an Account Freezing Order in the UK

Challenging an AFO requires a specific legal process. The grounds for challenge and the evidence required are important to understand.

Grounds for Challenge

How to Argue

No reasonable grounds

Suspicion was not objectively reasonable

Disproportionate

Order more restrictive than necessary

Wrong account

Order applies to wrong account

Legitimate source of funds

Money has innocent explanation

Procedural defect

Application did not comply with requirements

Delay

No forfeiture applied for within reasonable time

The Application to Vary or Discharge

Section 303Z9 POCA 2002

Where made

Magistrates’ court that made order

Who can make it

Account holder; anyone affected

What you must show

Grounds for variation or discharge

Evidence

Must provide evidence supporting grounds

Hearing

Usually listed for hearing

Both sides heard

Enforcement authority can respond

Proving Legitimate Source of Funds

Key Evidence

Employment records

Payslips; P60; bank statements showing salary

Business accounts

Legitimate business income

Tax records

HMRC records; tax returns

Property transactions

Proceeds of house sale

Inheritance

Documentation from estate

Gifts

Evidence of donor; their means

Investment returns

Brokerage statements

Benefit of the doubt

Any credible explanation raises doubt

What Makes a Strong Challenge

Evidential Strength

Clear paper trail

Documents showing origin of funds

Consistent with account history

Income matches lifestyle and deposits

No contradictory evidence

Nothing pointing to criminal source

Expert evidence

Forensic accountant if complex

Early action

Challenge promptly; do not wait

Appeal to Crown Court

Section 303Z16 POCA 2002

If magistrates refuse

Can appeal to Crown Court

De novo hearing

Fresh consideration

Both sides again

Full hearing

Costs

May be ordered

Time limit

Must act promptly

Can You Apply for Living Expenses From a Frozen Account?

Yes. One of the most important provisions is the ability to apply to the court for funds to be released for reasonable living expenses and legal costs.

Living Expenses Application

Section 303Z9 POCA 2002

Who can apply

Account holder

What can be released

Reasonable living expenses

Legal costs

Also included

Court decides

What amount is reasonable

Not automatic

Must apply; show need

Enforcement authority

Can oppose; but courts generally sympathetic

What Counts as Living Expenses

Examples

Rent or mortgage

Basic housing costs

Utilities

Gas; electricity; water

Food

Reasonable food costs

Essential transport

Getting to work; medical appointments

Medical costs

Prescriptions; treatment

Legal costs

Solicitor fees for challenging AFO

What Does Not Usually Qualify

Examples

Luxury spending

Holidays; expensive restaurants

Non-essential purchases

New cars; luxury goods

Business expenses

May be considered separately

Discretionary items

Non-essential spending

Practical Steps for Living Expenses

Process

Instruct solicitor

Application made by solicitor

Prepare schedule

Monthly expenses listed

Supporting documents

Bills; rent agreements; payslips

Application to court

Formal application

Enforcement authority response

Usually served on them

Hearing

Court considers application

Release of funds

If granted; account unfrozen to extent

What Is an Account Forfeiture Order?

An Account Forfeiture Order (AFO) is the permanent seizure of funds from a frozen account. It can be made without a criminal conviction, using only the civil standard of proof.

Forfeiture vs Freezing

Key Difference

Freezing order

Temporary; preserves funds pending investigation

Forfeiture order

Permanent; takes money from you

Standard

Both civil: balance of probabilities

No conviction needed

Forfeiture without criminal prosecution possible

Can challenge

Both orders can be challenged

Section 303Z14 POCA 2002

Forfeiture Application

Who applies

Enforcement authority

Court

Magistrates’ court

Standard

Balance of probabilities

What must be shown

Money is criminal property or intended for use in crime

Your right

To oppose; present evidence; attend hearing

If granted

Money permanently transferred to Consolidated Fund

What Should You Do If Your Bank Account Is Frozen?

Step 1: Do Not Panic, But Act Immediately

Why this matters: An AFO is a serious legal matter but it does not mean you are guilty of anything. However, time is critical. The order may have been made based on incomplete information, a misunderstanding, or a false allegation. Acting quickly to instruct a solicitor and gather evidence of legitimate funds gives you the best chance of challenging the order and recovering access to your money.

Step 2: Instruct a Specialist Solicitor Immediately

Why this matters: AFO proceedings are civil proceedings under POCA 2002 with specific procedural rules. You need a solicitor experienced in financial crime, asset recovery, and Proceeds of Crime Act proceedings. This is not general criminal defence work, it requires specialist knowledge of the civil recovery regime, forfeiture proceedings, and the specific legal tests that apply.

Step 3: Obtain a Copy of the Order

Why this matters: You are entitled to receive a copy of the Account Freezing Order. The order will identify the court that made it, the grounds relied upon, the account affected, and the duration. Understanding exactly what has been ordered is the first step to challenging it effectively. If you have not been served with a copy, your solicitor should request it immediately.

Step 4: Gather Evidence of the Legitimate Source of Your Funds

Why this matters: The most effective challenge to an AFO is demonstrating that the money in the account has a legitimate, lawful source. Gather all available evidence:

Payslips, P60s, bank statements showing regular salary deposits

Tax returns and HMRC records

Property sale proceeds documentation

Inheritance documentation

Business accounts and invoices

Any other records showing where the money came from

The stronger and more complete this evidence, the stronger your challenge.

Step 5: Apply for Living Expenses and Legal Costs

Why this matters: If the frozen account contains the money you need for daily living, you can apply to the court for funds to be released for reasonable living expenses and to fund your legal representation. Your solicitor will prepare a schedule of expenses and make the application urgently. Courts generally recognise that people need access to money to live, and this application should be pursued as a matter of priority.

Step 6: Challenge the Order Formally

Why this matters: An application to vary or discharge the AFO under Section 303Z9 POCA 2002 is the primary mechanism for challenging the order. Your solicitor will prepare the application, gather evidence, and represent you at the hearing. If the magistrates’ court refuses the discharge application, there is a right of appeal to the Crown Court. Do not simply accept the order — challenge it.

Frequently Asked Questions

How long can police freeze your bank account UK?

An Account Freezing Order initially lasts for up to 2 years, and extensions can be granted by the court. There is no statutory maximum on the total duration — in complex investigations, accounts can remain frozen for several years. During this period, the enforcement authority may apply for an Account Forfeiture Order, which would permanently take the money. If no forfeiture order is obtained by the end of the AFO period, the funds must be released.

Can the police freeze your bank account without telling you UK?

Yes. Account Freezing Orders are almost always obtained without notice, meaning the court makes the order before you are informed, giving you no opportunity to object in advance. Your first indication that your account has been frozen may be your bank card being declined or a transfer being blocked. You must be served with the order after it is made and then have the right to apply to vary or discharge it.

What should you do if your bank account is frozen by police UK?

Instruct a specialist solicitor immediately, obtain a copy of the order, gather evidence of the legitimate source of your funds, and make an urgent application for living expenses. Do not ignore the order or assume it will resolve itself. Challenge it formally through an application to vary or discharge under Section 303Z9 POCA 2002. The longer you wait, the harder it may become to gather evidence and the greater the risk that forfeiture proceedings are initiated.

Can you still pay bills if your bank account is frozen UK?

Not from the frozen account without a court order. Once an Account Freezing Order is in place, you cannot make payments from the affected account. However, you can apply to the court for funds to be released for reasonable living expenses, including rent, utilities, food, and essential transport. Your solicitor can make this application urgently. You should also consider whether you have other accounts or resources that can meet immediate expenses while the application is processed.

What is an account freezing order and how does it work UK?

An Account Freezing Order is a civil court order made by a magistrates’ court under Section 303Z1 of the Proceeds of Crime Act 2002, which prohibits you from withdrawing or dealing with the funds in a bank or building society account. It is obtained without notice by an enforcement authority such as the police, NCA, or HMRC, on the basis of reasonable grounds to suspect that the funds are criminal property. It does not require you to have been charged with any offence. It initially lasts up to 2 years and can be followed by an Account Forfeiture Order permanently removing the funds.

How do you get your bank account unfrozen after a police investigation UK?

By making a formal application to the magistrates’ court to vary or discharge the Account Freezing Order under Section 303Z9 POCA 2002. You must show grounds for the discharge — most powerfully, that the money in the account has a legitimate source. Your solicitor will prepare and present the application, supported by evidence of legitimate funds. If the application is refused, there is a right of appeal to the Crown Court. If no forfeiture order is obtained, the funds will be released at the end of the AFO period.

This website uses cookies to ensure you get the best experience on our website.SettingsACCEPT

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.